Last week I gave a presentation about the ‘big picture’ to a gathering of government officials in Wellington. I talked about China’s economy and financial market volatility, rather on-the-money topics given this week’s global stock-market meltdown! Here is a potted-version of that presentation.

Global outlook

When anybody says ‘global economy’ they’re really talking about three economies: the US, China and Europe. 4 at a push if we include Japan.

On one level, the story of the global economy is a very simple one: output in the world’s second largest economy China is beginning to grow more slowly and that is impacting on everyone who trades with them. It is leading to falling commodity prices, reduced export forecasts, lower interest rates and generally quite a bit of business doom and gloom. New Zealand is exposed because it not only trades a lot with China, it trades a lot with countries which trade with China (eg Australia and south east Asia).

It wouldn’t be so bad but other large economies are stuck in the doldrums too – While Europe and the US are both expected to grow more quickly than they have in recent years, that’s not saying much.

| Annual growth %pa | 2013 | 2014 | 2015 | 2016 |

| World Output | 3.4 | 3.4 | 3.5 | 3.8 |

| Advanced Economies | 1.4 | 1.8 | 2.4 | 2.4 |

| Emerging Markets | 5.0 | 4.6 | 4.3 | 4.7 |

Source: IMF World Economic Outlook April 2015

Business confidence is ‘Flagging’ said the ANZ in its business outlook report in July. No surprise there.

WHATS UNUSUAL IS CHINA

What’s unusual about this situation is that in the past large developing countries – and China is the largest – grew quickly and steadily. They provided a buffer during the business cycles of the developed world. If demand in the US became a bit weak, US products could be sold into the ever-expanding Chinese market and US businesses could stay afloat.

The news out of China suggests that buffer is not as robust as it once was. It can’t keep acting as a sponge for the rest of the world’s economic over-spill.

The World Bank tells us that after growing steadily at more than 10% a year for three decades, China’s output growth is slowing to 7% and is expected to dip under 7% by 2017.

When you’ve no longer got a country like China acting as a buffer for the world’s economic ups and downs, exchange rates and interest rates have more work to do. They send signals to businesses, investors and consumers that lead to adjustments in behavior that eventually moderates business cycles within each country.

So because the world no longer has the China buffer available to it, the peaks and troughs in exchange rates and interest rates may be greater than in the past. Ups and downs could be more magnified than we’ve experienced in quite a while.

New Zealand doesn’t seem particularly well-equipped to understand, prepare for and benefit from developments in China. Economists could do a much better job than they seem to be doing.

ECONOMISTS DON’T HAVE A GOOD UNDERSTANDING OF HOW THE CHINESE ECONOMY BEHAVES

Economists are not typically trained in central planning – they’ve come from an environment where economic decisions are typically made in markets fuelled by private self-interest. Their tools are uniquely inappropriate when self-interest isn’t the driving factor in decision-making.

Inevitably economists seem to moan about the Chinese government not understanding markets, but that’s really unhelpful.

Last week economist Paul Krugman, who is a Nobel-Prize winner and regular columnist at the New York Times, had this to say:

Aug 14th Bungling Beijing’s Stock Markets

“The common theme in these wild policy swings is that China’s leadership keeps imagining that it can order markets around, telling them what prices to reach. And that’s not how things work.”

I think he’d do well to focus on the reality of what is in China, and try and understand that, rather than bemoan the fact China doesn’t fit his definition of what an economy should be.

Despite decades of experiment and reform, the Chinese government retains effective control over a considerable part of the economy. There are still 155,000 SOEs for example. State control is especially evident in the financial sector. There are four large state-owned banks that dominate, and they’re subject to close control. For example, almost 95 per cent of all the loans made in China are controlled by the central government. So the government largely orders the financial sector around – that’s how things work in China.

Economists like Krugman need a framework for understanding the process of transition from ‘communism’ – impatiently applying to transitioning economies analytical tools that are only appropriate for market-based economies isn’t doing anyone any favours.

THERE IS NO GREAT DATA ABOUT CHINA

And even if we do be more open minded and get a better framework for understanding China, there is the ongoing problem of getting reliable data. Heaven knows, it’s hard enough getting accurate data on a tiny country like NZ, imagine the practical problems in doing it for China. It’s always been an issue for China.

And of there are the ongoing (naive in my view) whispers about official data and unofficial data – of course there are different data sets – there always has been. Without the discipline of a voting public demanding honest statistics, where would the pressure come from?

And let’s be honest, even in our democracy, even when data is robustly collected the messages from it can be twisted beyond recognition in the hands of skillful spin doctors.

So, in summary, we lack a good understanding of China. And that leads on to a second problem. We don’t understand how China affects us.

WE DON’T UNDERSTAND HOW CHINA AFFECTS US

We seem obsessed with looking at foreign trade: imports, exports, dairy prices. But capital flows are hugely important too, but overlooked.

The economic policy tools available to the Chinese authorities are evolving but they are still not as flexible as those we’ve become used to here. Controlling credit growth has always been a problem in China and still is.

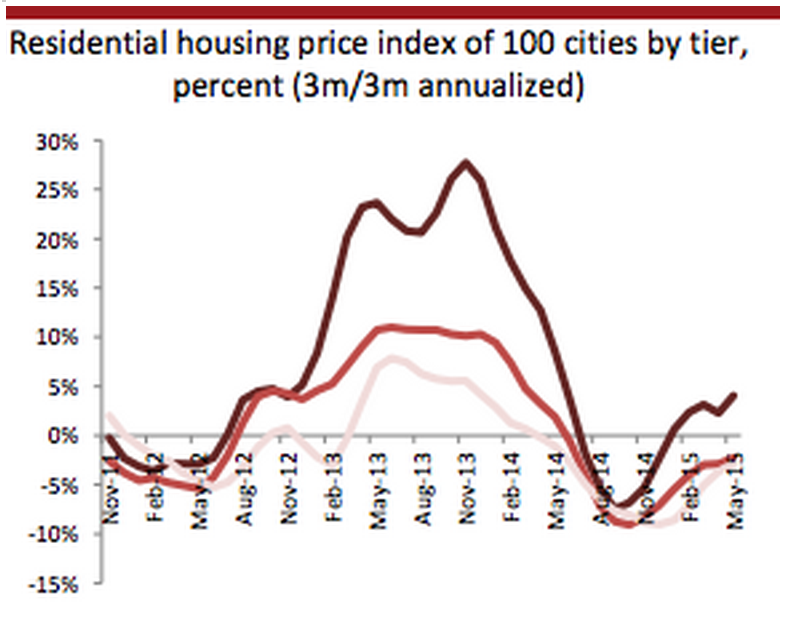

Because the banking sector remains largely undeveloped, the government has rather imprecise monetary policy tools available to it. During 2012-early 2014 credit growth was excessive in China and it led to a domestic housing bubble.

The government subsequently crunched credit growth, with led to falling house prices, but has recently begun easing again. House prices rose strongly, fell sharply and are now rising again. The local stock market showed a similar boom and bust profile.

To complicate matters, during 2013, there was an easing of controls over investment abroad by Chinese companies – which made it easier for Chinese companies to invest overseas if they wanted to. Until then, non-sanctioned investment occurred but through informal channels.

And for the first time in 20 years China officially devalued the RMB last week (it has an informal peg against the USD).

So initially the credit boom, and then looser foreign exchange controls, led to unprecedented capital flows from China to other markets – the US, the UK, Canada, Australia ….. and I would argue NZ (although we have no comprehensive data….). In July the World Bank reported that capital outflows from China are still increasing sharply. Now of course, further fuel is being added by fears of further weakness in the RMB.

There is a common pattern to the capital flows from China – the capital isn’t just flowing into stock markets and bank deposits in other countries (these are usually popular because they’re well regulated and it’s easy to cash up again) but into property.

“Asian investors bet on US real estate” (CNBC: Oct 2014)

“Chinese buyers looking for Australian property ‘bling’ “ (BBC July 2015)

“China’s rich seek shelter from stock market storm in foreign property” (Guardian July 2015)

I want to make the point that what I am talking about here is capital flowing out of China, not people – the issue of capital flowing from China is a separate issue to migration.

What we have is a situation of China’s financial assets becoming globally mobile. It could occur with or without an accompanying lift in migration from China. It happens to be the case that we’re receiving higher levels of migration too.

NZ HAS BEEN CAUGHT NAPPING

As a country, we’ve been caught napping.

– We were not expecting capital to flow here from China (why not?);

– If we’d been asked we probably would have expected it to enter our stock market or our companies not our property market (although there were warning signs from other countries);

– We didn’t even have a system for monitoring direct capital flows into our housing market.

– We’re not even talking about the issue sensibly. We’re allowing our media to drive the debate and they are making the mistake of muddling capital inflows from China with people inflows (migration) – as a result anyone who questions the benefits of having sizeable foreign capital inflows into New Zealand property gets accused of being anti-migrant and inciting racism.

We need to start thinking quickly about the effects on New Zealand of China’s economy. We need to move beyond a focus on dairy prices and exports. What about unprecedented capital flows from China? Are the flows permanent or just hot money? Are we making the best use of the money? What are the social consequences of escalating house prices and how can we mitigate those?