With an aging population and people living much longer than they did we are in a position of having more people not working than working- which is a problem because it is working people that pay for super. In addition with superannuation indexed to wages (the amount of super paid increases as wages increase) we have a bit of a problem with money. The way we are going our national debt is going to blow out a lot (2 times our national income actually) and we will have to borrow even more to pay for anything else. Which means a huge squeeze on infrastructure, social spending, health, and education. So the Government has popped its head of the sand briefly and now says that in 20 years we will increase the age of superannuation to 67. Winston Peters, the official champion of the elderly, well he is ok with all the cash going to those over 65 and the rest can go hang.

Rising Costs

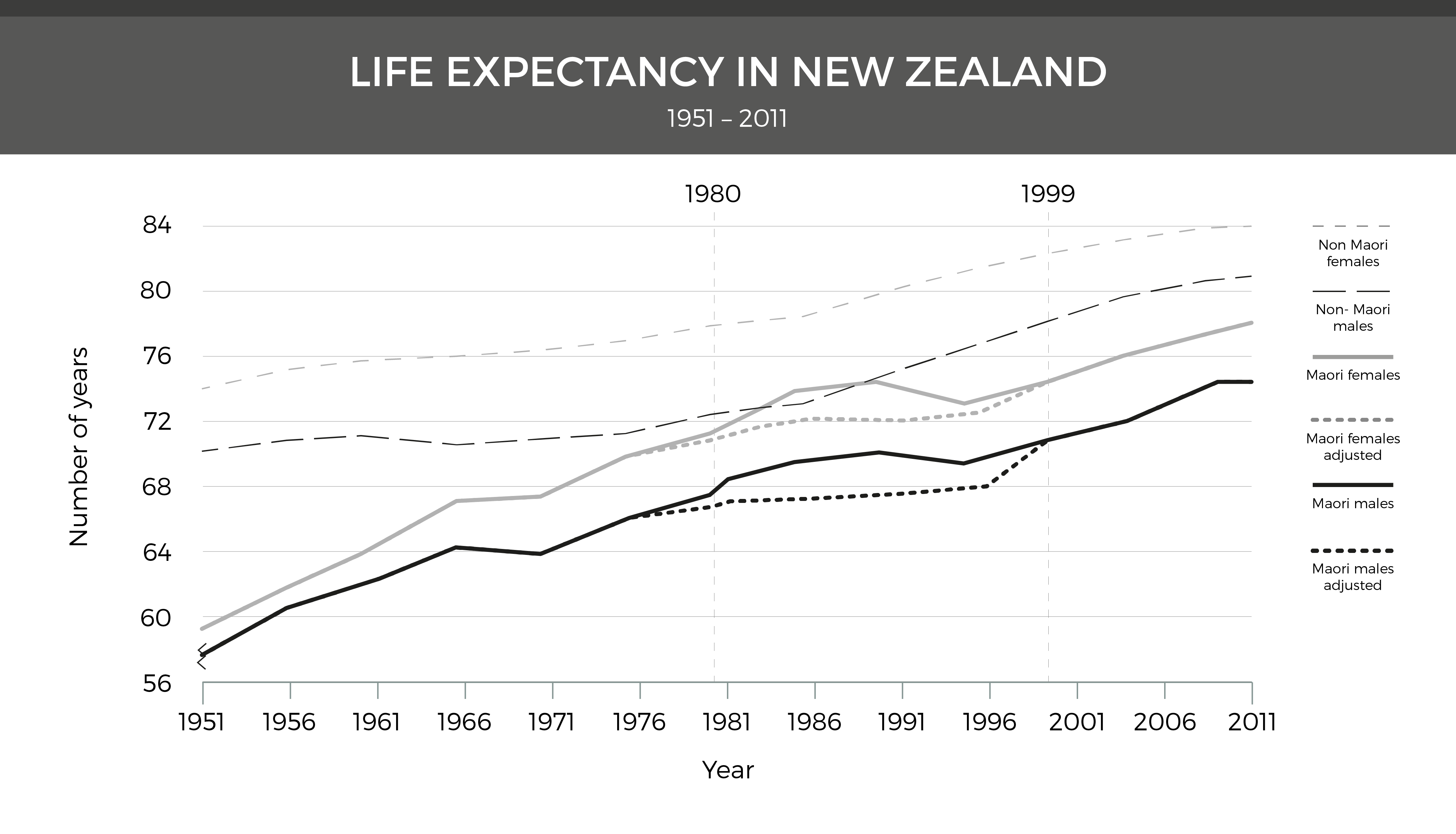

By the time most of us retire the taxes we paid over our lifetime would have been well spent on other Government services we all use. There is no nest egg waiting for us with our nametag attached to it. Rather the people working while we are retired are paying for our Superannuation. If you think about it, it has a “nice circle of life” aspect to it. The problem is that when there are more older people than working people and they are living longer than ever then things get pretty dicey. When universal superannuation was first introduced in the 1970’s the average lifespan was about 75 – look at where we are at now in terms of life expectancy- that is a lot more money to pay to a person over their retirement. As people live to over 100 years increasing numbers of people will get Superannuation for longer than they worked.

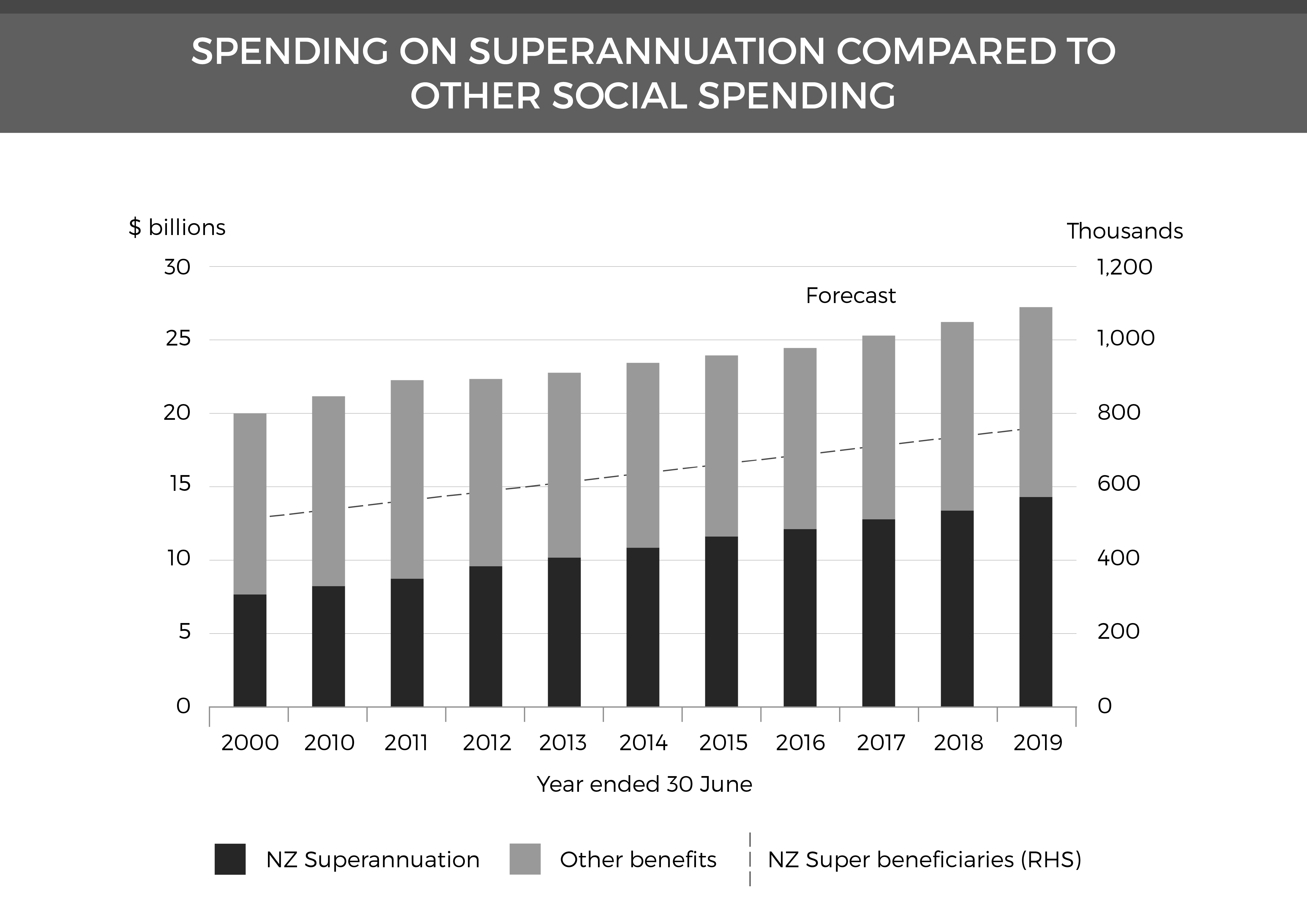

Below are the costs of Super modelled just for the next few years. We can see that as we spend more of our finite supply of tax other spending has to be pared back. Spending for example on children. If we don’t invest in children when they are young then we don’t get adults with all the skills we need and the wellbeing they need to be productive, then collectively we don’t have the productive, wealthy society we need to support older people in their retirement. Which is kind of ironic. Something then does need to be done.

So lets look at raising the Superannuation age to reduce costs and consider what the impacts might be.

Raising the Age Works for the Well Off & Healthy

In the graph above on life spans, you will see that Maori men and women have shorter life spans than Pakeha men and women. They also earn less over their lifetime, and are more likely to work in manual or physical industries – the traditional blue-collar worker. Raise the age of superannuation and those who get hits hardest are those who are least able to accommodate it – because we have a problem with equality in New Zealand.

Lets talk about Manu.

Manu is a childcare worker; she is qualified but is paid quite low wages. She took time out of work to raise her family, and later she took time out to look after her elderly parents. Manu has made a huge contribution to New Zealand society. The unpaid caring work she did has measurable value. Unpaid work contributes at least $40billion to our economy each year according to Statistics New Zealand – women do 65% of this unpaid work. Women tend to do their unpaid work during the years they could be working (men tend to do it after retirement). Manu has less saved at retirement than her friend Big Ted because she earned less and because she took time out to care for others. She is tired at 65, she has done a lot of physical work with small children and older people over her life, yet she will need to continue to work for another 2 years to get her Superannuation, which she will relay on to pay her on-going costs. Manu will in all likelihood die before Jemima (her Pakeha friend) and so will receive less superannuation overall. Manu also has less wealth as a lower income New Zealander, and has not been able to buy and pay off a house in her lifetime. At 65 she is still paying for her rented accommodation and will continue to do so until her death. This sucks for Manu- a woman who has contributed in many positive and productive ways to New Zealand society over her lifetime. Ultimately, Manu’s wellbeing (or lack of it) is also going to be expensive for New Zealand in terms of health care and social costs.

Now Lets talk about Big Ted.

Big Ted is from a comfortable middle class family. He has worked hard like Manu. He worked in middle management and during the years when his kids were young, and his partner Humpty took time out of his career to raise them, he worked his way up the income and experience ladder. By the time he was 42 he was a CEO. He was paid very well. Nearing retirement age he now sits on a few boards and has a very comfortable retirement fund, plus two fully paid off investment properties. At age 65 Big Ted decides he won’t retire, he loves work and has a lot to contribute still. Ted continues to sit on a number of boards well into his 70’s – which he is paid well for. Big Ted collects his Superannuation payment at 67, but having to wait those additional two years makes little difference to him. Each year Humpty and Big Ted use their superannuation to go on a motorbike trip somewhere exotic. Big Ted is likely to live a long life- the wealthy better off tend to live longer than those who have experienced a lifetime of economic doldrums. Retirement is good to Big Ted and he can easily absorb a change in age of eligibility.

What other options are there to pay for our Super bill that does not suck for Manu?

We could income test it (or put a higher tax rate on high earnings over 65). This is unpalatable to many, comes with bureaucracy and could miss a lot of people who minimize their incomes. It could hit those people who still need to work because they have to pay for their housing for example hard. It may also deincentivise work in older people and we want them contributing in an aging population.

We could asset test for superannuation. This is also unpalatable, but mainly to the wealthy, it comes with some bureaucracy but gets to peoples’ real wealth base better and means people cannot minimise their income and still claim super.

We could close tax loopholes that incentivise investment in unproductive things like housing and encourage people to invest in productive enterprise instead. Greater productivity will help, but with super tied to wage increases this will mean we still have a bigger super bill to pay. We could look to index it to inflation instead.

We could increase immigration and population size and bring in more

skilled workers to pay the bill. This approach increases our diversity, keeps up with the need to have younger workers helping support the elderly, but remains controversial in some communities in New Zealand.

We could build our productive economy with greater investment in children. Investing in the children we do have is really important to ensure when children become adults they have everything they need to thrive and hence support older people. We tend in this country to treat children a little like cicadas. They remain out of collective sight and out of mind (and responsibility) during their key development years. We then complain when they emerge and make noise that we don’t like.

Investing in children (all children not just the so called ”vulnerable” ones) will help with our productivity issue, but we would still need to do some if not all of these other things.

It is up to New Zealanders how they want to manage this looming crisis, if we don’t want to create even more problems for ourselves, looking to ensure the changes we make support those who need it most seems like good long term governance.