Housing boom figures should convince government to put its hands back on the steering wheel

Guest post by Bernard Hickey

There’s a tipping point for any pragmatic policy-maker where the facts change to such an extent as to render any existing strategy redundant.

Depression-era economist John Maynard Keynes explained his change of mind on monetary policy after the Depression thus: “When the facts change, I change my mind. What do you do, sir?”

This week New Zealand reached that tipping point when it became clear the facts have changed and it’s time for the government to change its mind.

The facts on the economy are so demonstrably different to expectations that the government, the Reserve Bank and voters should reassess the direction embarked on four years ago when the National-led government took power and committed itself to a ‘hands-off’ approach to monetary policy, the big Tax switch, and a plan to return the budget to surplus by 2014/15.

Thursday’s Household Labour Force Survey showed unemployment blasted through expectations to 7.3%, its highest level since 1999. Employment actually fell 8,000 when it was forecast to rise by the same amount. Prime Minister John Key was clearly surprised to the point where he even suggested policy makers should rely on his anecdotal evidence rather than Statistics NZ’s figures. Finance Minister Bill English was sensibly more subdued.

Friday’s figures from the Real Estate Institute of New Zealand (REINZ) showing median houses hitting record highs in October both nationally and in Auckland simply reinforced that the economy is heading off in exactly the wrong direction.

And it’s not a new direction. Cheap and easy credit along with supply shortages are inflating house prices beyond the reach of young families wanting to own their home, particularly in Auckland.

The median house price in Auckland rose 14% in October from a year ago. Sales volumes rose 44% in October from a year ago in Auckland. The median price rose 5.8% in October from a year ago and volumes rose 32.6% from a year ago. The market is so hot the REINZ even bragged that the market had ‘roared into life’ in October.

Party like it’s 2007 with a jobless rate like it’s 1999

We seem to be back where we started in late 2007.

A hot housing market is forcing the Reserve Bank to keep the Official Cash Rate higher than it would otherwise like. This in turn keeps upwards pressure on the New Zealand dollar, which makes our manufacturing exporters less competitive. That in turn costs jobs, many of which are high wage jobs.

Key may be seeing anecdoctal evidence of job creation in Auckland, but just this week Christchurch electronics manufacturer Dynamic Controls proposed shedding 60 jobs and high tech exporter Rakon announced it would cut 60 jobs and move production to China. Solid Energy and Tiwai Point announced hundreds of high paid job losses last month, which have yet to be registered in the jobs figures. Jobs are being created, but they are in lower value services sectors such as healthcare, big box retailing and restaurants that are not subject to international competitiorn, or are higher value jobs in real estate and financial services. That means fewer mine workers and factory workers and more Warehouse checkout operators and real estate agents.

The high exchange rate is sending a clear signal to consumers and businesses alike: buy imports, convert businesses from exporting to importing and employ people involved in real estate investment and financial services. The record low interest rate and a loosening of lending controls for mortgages is convincing a whole generation of borrowers that they can afford their dream home if only they can outbid their rivals by borrowing as much as they can with a 5% deposit and interest rates at 5%. The Reserve Bank is forecasting their rates will only rise around half a percent in the next two to three years and the Government’s response to the Productivity Commission’s Affordability Inquiry insures few new houses will be built any time soon.

Banks are offering free tablet computers, NZ$1,000 cash back bonuses, discounts on legal fees and low-doc loans, just as they were in 2007. The Financial Stability Report this week (figure 4.6) showed another easing of lending rules for households in the last six months and banks are at it hammer and tongs to win over disgruntled ANZ and National customers dislodged in their merger.

The messages are as clear as a bell. Gear up, buy property and you can’t lose. Don’t bother investing to export. You’re much better off borrowing to import because foreign investors will keep lending to New Zealand forever and we can always sell off more businesses, state assets and land as well to make sure we fund our current account deficit. Leverage up and just wait for the tax free capital gains to fall into your lap. It’s much easier than building or producing something to export it.

It wasn’t supposed to be like this

The National-led government began with such promise and ambition. It wanted to turn around the economy’s obsession with property investing and reverse the decline in the productive and exporting sectors.

The big tax switch of 2010 was designed to discourage consumption by increasing GST and encouraging production and investing by lowering corporate and high income tax rates. This was supposed to switch the incentives. The introduction of tougher tax rules for residential property investors was also supposed to knock the rental propety obsession on the head.

The aim was to reduce the indebtedness of the household sector and the vulnerability of the economy by earning plenty of foreign exchange revenues to pay high wages and invest in export businesses. It was supposed to create a virtuous circle.

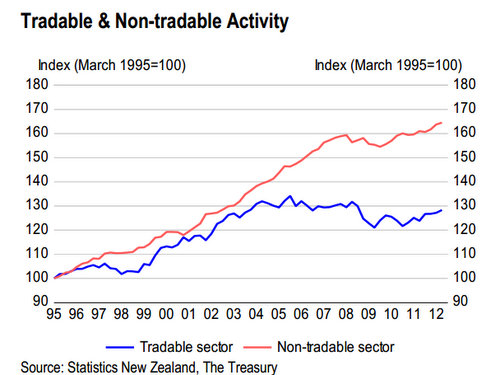

Instead, the gap between the tradeable sector (including exporters and those competing with imports) and the non-tradeable sector (financial services, government, real estate and retailing) is even wider now than it was in 2008.

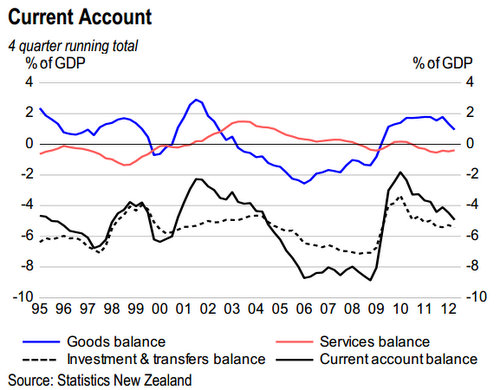

New Zealand’s net foreign debt is only marginally lower, largely because of reinsurance payments for the Christchurch earthquakes. The ‘foreign drain’ of interest payments on foreign debt and dividends on foreign owned assets remains embedded in the economy.

Even Treasury is forecasting the current account deficit to rise to 6.7% of GDP by 2016 from 3.8% in 2011. New Zealand has actually been running a goods and services trade deficit this year. That’s before the interest payments and dividends to foreign owners. Simply from the four banks alone, their profits rose 12% to NZ$3.2 billion or about 1.6% of GDP this year. See more here in Gareth Vaughan’s article.

Yet the New Zealand dollar is still 15% over-valued according to the IMF and above where it was in 2007. The usual economic theory says the exchange rate will act to help balance a current account deficit. It should be falling to close the gap.

The usual theory

The trouble is the theory of free floating exchange rates responding to commodity prices and economic fundamentals such as current account deficits has been blown out of the water by the Global Financial Crisis and the various responses of intervening and printing by central banks and governments.

Central banks and governments in six of the top 10 currencies by volume are intervening directly or indirectly in their currencies. The United States, Japan, the European Union, the Bank of England, Switzerland and Hong Kong have all either engaged or threatened Quantitative Easing (Money Printing) to try to boost their economies and weaken their currencies over the last year. The other four in the top 10 who aren’t intervening in their currencies are Canada, Sweden, Australia and New Zealand.

Capital flows, much of it printed by central banks at 0% interest rates, are now cascading around the world to those currencies with higher interest rates (than 0%) where money is not being printed. Much of this money is flowing into property sectors and stock markets. At least some of the demand for central Auckland property is from Asian investors able to source funding in their home countries at much less than the 2.5% of our Official Cash Rate.

Many countries have acted to stop these unnatural capital flows from damaging their productive sectors. Some have imposed capital controls. Others have printed money to buy foreign currencies to stop their currencies from rising. FT.com reports here that Switzerland’s latest interventions have been successful in capping the rise of the franc.

They all have a similar problem. If they cut interest rates to give some relief to their productive sectors and weaken their currrencies, this would just encourage more leveraged investment in property, risking the financial system blowing up another asset bubble that destabilises the financial system. The last thing they want to do is create another bubble of Too Big To Fail banks and unsustainable house prices.

There is another way

So central banks and regulators have acted to cauterise their property markets from the blunt instruments of monetary policy. They’ve used so-called ‘macro-prudential tools’ to slow down lending into these property markets to either avoid having to hike official cash rates or allowing them to cut rates. Here’s an IMF paper on ‘macro-prudential tools’ to show how it’s being done elsewhere.

Canada’s Minister of Finance announced in June this year that mortgages with government-backed insurance would be limited to 80% of their home value (down from 85%) and be cut to 25 years (from 30 years). Any borrowers’ maximum debt service ratio would be also be limited to 44% of income and borrowers would not get government-backed mortgage insurance on houses worth more than C$1 million. In March Canada’s Office of the Superintendent of Financial Institutions announced it would limit home equity lines of credit (HELOC) to 65% of the value of a home and would not provide mortgage insurance for HELOC loans. See more here at The Global Mail.

Last week the Bank of Israel imposed a loan to value limit for first home buyers of 75%, a limit of 70% for existing home buyers and a limit of 50% for rental property investors. See the Bank’s directive here. At the same time it announced a surprise cut of 25 basis points in its Official Cash Rate to 2% to help support its economy and offset the impact of a rise in its currency. Israel’s house prices have risen 2.9% in the last six months.

But back in Orthodox land…

Meanwhile, New Zealand house prices, as measured by the REINZ’s stratified index that takes out some of the ‘noise’ from more sales of expensive houses, rose 3.5% in the last 3 months and 6.9% in the last year.

If only the Reserve Bank could slow down the housing market with macro-prudential tools instead of the Official Cash Rate.

The Reserve Bank is investigating using such tools, including Loan to Value Ratio limits and things such as ‘counter cyclical capital’ buffers, which would require banks to hold more capital at times of strong economic growth.

But this work is still only investigatory and the Reserve Bank has yet to agree a Memorandum of Understanding with the Government on how and when it would use such tools. New Governor Graeme Wheeler even said he wouldn’t use the tools even if he had them….yet. See more here in this piece with a video of Wheeler’s views. Previous Governor Alan Bollard looked at using them in 2006 and decided against it. He reiterated last month he was opposed to using them.

It beggars belief. So when would the Reserve Bank and the new Governor use them? Is a 14.4% rise in house prices in the country’s biggest real estate market in one year (past tense) not enough? House prices rose 3.5% nationally and 7.7% in Auckland in the last 3 months. That’s twice as fast as the growth being seen in Israel. Also, inflation is running below the Reserve Bank’s own target band of 1-3% and below the 2% average that he has agreed to focus on in his new Policy Targets Agreement. I

Why won’t he act? Surely he’s not asleep at the wheel(er)?

….And back on Planet Key

In the meantime John Key has pledged to stay the course with the government’s ‘hands off’ strategy for the currency and the Reserve Bank Act, and will stick to the plan to get the budget back into surplus by 2014/2015. This implies a fiscal policy tightening of around 4% of GDP over the next three years.

If the government is going to tighten by 4%, which part of the economy is going to expand by the same amount or more to avoid going into recession? It was supposed to be the private sector and, in particular, the export sector. That now looks very unlikely with a currency stubbornly over 81 USc and rising towards 80 Australian cents. It also looks unlikely with Europe in or near recession, China slowing from a 10% plus growth rates to closer to 7% and Australia slowing to under 3% growth.

So what to do?

If the government and Reserve Bank do acknowledge the facts have changed, then what should they do?

Here’s a few ideas in no particular order:

Introduce loan to value ratio limits similar to the Israeli ones – They are conventional monetary policy tools now and would avoid a whole new generation of borrowers getting up to their eyeballs in debt just before interest rates start rising again. They will also reduce the financial vulnerability of any banks were house prices to fall sharply because more equity means less chance of mortgagee sales.

Introduce counter-cyclical capital buffers – This would slow down bank lending growth in a much simpler way than an increase in the Official Cash Rate and doesn’t punish existing borrowers for the actions of those borrowing at the fringes. It would mean banks have to top up their equity, probably by not sending dividends back to their Australian parents. That would help reduce the current account deficit in a similar way to what happened in 2009 when banks agreed to pay higher tax rates. It would allow the Reserve Bank to cut the OCR and give relief to business borrowers, or at least offset any increase in interest rates imposed by bank shareholders to protect their profits given the higher capital requirements.

Increase the risk weightings and capital requirements for mortgage lending – This would force banks to slow mortgage lending and put aside more of their own capital to back these loans. It could be argued this would reduce the ‘over-weighting’ of New Zealand bank assets to one type of asset. Any investment manager will tell you that diversification reduces risks. Gareth Morgan has suggested such a move in his 5 point plan.

Introduce a land tax or capital tax or capital gains tax – This imposes a holding cost on land-banking property developers and transfers some of the easy wealth gains of the recent gains to non-property owners. It also evens up the playing field so that capital gains are taxed as much as income. Gareth Morgan’s Big Kahuna idea for a tax on capital is the simplest and most redistributive idea around.

The Central government and local government must urgently work together to build 50,000 new homes in Auckland and Christchurch – The combination of the market and local council regulation has clearly failed to deliver the affordable housing desperately needed to put some pressure downwards on house prices and make New Zealand an attractive place to live.

Rewrite the Reserve Bank Act to allow it to target other variables than inflation – These other targets should include a combination of the exchange rate, employment levels, the current account deficit, inflation and wages. Inflation targeting is now widely discredited overseas, yet the orthodox dominates at the Reserve Bank and Treasury.

Rewrite the Reserve Bank Act to allow it to buy government bonds directly from the government – This would allow the Reserve Bank to finance the government deficit once interest rates are cut to the lower bound of % and avoid deflation. It also removes the financing restriction for rebuilding Christchurch’s infrastructure and Auckland’s infrastructure, including housing. It may not be necessary just yet, but we’re not far off given the current trends with employment, inflation, the global economy and the budget deficit.

Run a deficit for longer – The government needs to abandon its budget surplus target for 2014/15. Moody’s has already said it would not downgrade New Zealand’s credit rating if this happened and last year’s credit rating downgrades by Fitch and Standard and Poor’s did not lead to interest rate increases.

This opinion piece was first published by Bernard Hickey on Interest.co.nz and is reprinted here with permission.