Some claim that Uber has joined the ranks of other tech companies like Google, Apple and Facebook in minimising their New Zealand tax obligations. How Foreign Corporates Avoid Paying Tax in New Zealand and what we can do about it?

The tax base needs to be comprehensive if it is to be fair and efficient. A broad base enables personal income tax rates to be kept as low as possible and, if there are no gaps in the tax base, decisions are made on the basis of economic return, not the incidence of tax.

Business income is part of the tax base and New Zealand is one of the few jurisdictions that operates imputation credits to ensure that the profits distributed to shareholders (not all profits are distributed) aren’t taxed twice. Corporate tax provides 25% of the overall income tax revenue, PAYE provides 60%, and other personal income tax (for example earnings of the self-employed and term-deposit holders) provides 15%. So corporate tax is significant and protecting the integrity of the corporate tax base is important on both fairness and efficiency grounds.

How foreign corporates minimise their tax bill

Foreign-owned or partly foreign-owned firms operate in New Zealand and are expected to pay New Zealand tax on the profits they make here. If such firms were exempt income tax (paying tax only at home where tax rates may be lower) foreign firms would have an unfair tax advantage over domestic firms.

But clearly foreign-owned firms also pay income tax in their home tax jurisdiction. Double taxation agreements between countries have been developed to ensure that firms only pay tax on any particular dollar of profit once. Such firms are able to get a ‘credit’ from their home tax collector for the tax already paid overseas. But these double taxation arrangements only work if the tax regimes between countries are broadly similar – otherwise there is an opportunity for firms to arbitrage different tax regimes, meaning they would tend to gravitate their home office to the lowest tax rate jurisdiction they can find. Double taxation arrangements therefore are not universal – they only come about between jurisdictions of similar tax impost.

theglobalmail.org

This ‘ideal’ cross border tax arrangement has over recent decades, come under duress, as countries have deployed all manner of means to provide lower effective tax rates to companies that base themselves in their jurisdiction. Their motive is to attract as much foreign direct investment (FDI) as they can. These measures extend far beyond the obvious ‘weapon’ of lower tax rates and include subsidies, tax exemptions, regulatory assistance, and other means which disguise the effective assistance being given. For multinational corporations there has evolved a ‘game’ wherein they have been inclined to hold auctions between countries for the privilege of hosting their head office – with the winner being the host with the most effective concessions.

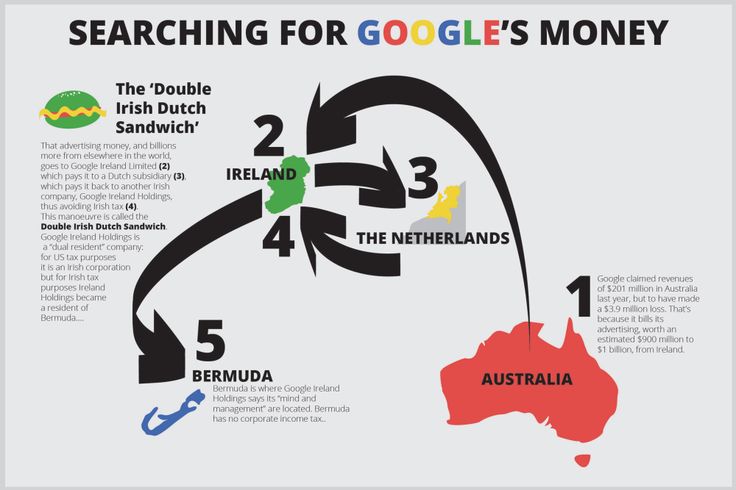

Competition between countries to attract FDI has intensified over recent decades with countries like Ireland and Switzerland being the most aggressive with corporate tax rates of 12.5% and 8.5% respectively. In addition to lowering the corporate tax rate from 40%, Ireland also has allowed the “Double Irish” technique where a multinational would set up a subsidiary in Ireland, route profits from its other offshore operations to that subsidiary which would then, more via transfer pricing, transfer those to a second Irish subsidiary that had its headquarters in a tax haven. In 2014 the Irish government bowed to pressure from other countries and began phasing in a requirement that all companies in Ireland pay Irish tax (albeit at the low 12.5% rate).

However at the same time as Ireland’s leaders announced the end of the “Double Irish” they introduced a new tax provision that allows companies to pay no tax on income derived from patents, licences and other intellectual property. So surprise, surprise – multinationals operating in other countries have subsidiaries in Ireland that hold IP and charge big fees to the company’s subsidiaries in other countries – like in New Zealand.

In the face of this ‘race to the bottom’ in the taxation of multinationals, other countries have adopted aggressive tax regimes to attract foreign companies, albeit not via low headline rates. In the US for example the headline rate is 35% but the tax breaks are so extensive for corporates it ends up being much lower than that. The Netherlands and Luxemburg are also very active in this area.

The OECD estimates that anywhere between 4-10% of global corporate income tax revenue is being lost due to this unwarranted ‘race to the bottom’ for FDI.

What is being done internationally and is it enough?

The short answer is we should just get on with taking action here in NZ like Australia and the UK are. But if you are a tax lawyer and interested in why, read this section! Otherwise, scroll on…

International State of Play

These practices led to the establishment by the OECD in 2013 of BEPS – the Base Erosion and Profit Shifting project. This is an initiative aimed at producing a new international standard for the taxation of profits of foreign-owned firms. According to the OECD BEPS is aimed at “realign[ing] taxation with economic substance and value creation, while preventing double taxation”. If something emerges from BEPS it will be the first substantial renovation of the international tax rules in almost a century.[i]

There is considerable argument over whether a collaborative approach as per the OECD’s BEPS project will actually be effective in neutralising the taxation arbitrage that multinationals are conducting. Two countries in particular – Britain and Australia – have decided that the leakage is too significant to await international agreements. Their argument is that waiting for an internationally coordinated response is akin to the international efforts to get coordination on carbon emissions – struggling to move forward any faster than even a glacial pace. Meanwhile the multinationals are laughing and local firms in small, open economies like New Zealand are paying a high price. These firms operate under a competitive tax disadvantage that adversely affects employment and GDP. As well, New Zealanders miss out on the services higher tax revenues could provide or, alternatively, pay more in tax for existing services than they would otherwise.

So Britain and Australia have moved to unilaterally impose their own tightening of rules around the conduct in their countries of foreign firms. There are risks of course of retaliation from other countries but presumably the rationale is that once an internationally coordinated effort is credible each country will join up. Meanwhile the damage must be halted.

The convention that has evolved over many decades is that income tax is liable in the country where a product or service is sold by the foreign firm. But a vexing issue arises – what are the appropriate costs to deduct from product sales in the jurisdiction in order to arrive at taxable profits? In New Zealand we have seen firms able to shift taxable profits beyond the New Zealand tax jurisdiction by claiming inflated costs – either interest payments incurred through taking on debt-heavy balance sheets (with the debt issued from related parties), or inflated (‘transfer’) pricing on their inputs (including IP, royalties, licences).

The challenge is how to address this tax arbitrage and bring to a halt the economic damage it imparts on countries where products are sold by foreign firms.

Should New Zealand act alone?

Given the scepticism that abounds around the OECD BEPS initiative, coupled with the economic damage being inflicted by the practices of the multinational corporations, how long New Zealand should allow the situation to persist? Should we just sit there and let the rorts continue until the OECD gets traction?

Tax professionals who earn fees from these aggressive corporate practices of avoidance may well say yes, harmonious treatment is vital. However there is considerable political opinion that such advice is sourced more in self-interest than in the national interest. I would suggest that New Zealand gets on with unilateral reforms, as the UK and Australia have done.

For credibility a tax regime must be seen to be fair; for efficiency it must be fair in reality. Having said that, it’s a two way street and there are plenty of New Zealand firms generating income abroad who should also be subject to effective taxation policies in foreign jurisdictions. So we should be prepared for any change to our tax eligibility practices to be responded to – at least by mirroring – elsewhere.

One argument the tax advisory sector is promoting is that multinationals should pay tax only in their home country – this is where the capital (especially intellectual capital) is located.[ii] But for the reasons outlined above if they face an easier tax burden in their home country, then they will be able to compete unfairly with local firms in higher tax jurisdictions. To the extent sales are made in the foreign market, the relevant costs associated with those sales should be deducted and the resulting profit taxed in the destination, rather than in the home country.

It is reminiscent of the historical arguments around ‘dumping’ – the business practice of selling products overseas at prices below those that apply in their home market. In dumping cases the strategy was to ‘buy’ foreign markets through the steep discounting, driving competitors out of business before raising prices to profit-maximising levels. In the case of tax arbitrage it is the home country’s taxation system that is buying the foreign market for the firm.

Our morbid dependence on foreign direct investment (FDI) has become inculcated in the culture of the tax discussion in New Zealand. We see it here in film industry subsidies, we see it in continual warnings from the Treasury (our government’s financial adviser) of “Armageddon” should these foreign corporates pay their fair share of tax. So long as New Zealand sacrifices fundamental principles around tax such as fairness to this craving for foreign investment, while at the same time not ensuring capital deployed in our economy isn’t used as efficiently as possible (the CCIT argument) then we will have an economy that is too dependent on the whims of multinationals. That is a feeble way to establish a society’s economic base – making it so vulnerable to the behaviour of foreigners. Treasury would be more fruitfully employed looking at ways to reduce reliance on foreign capital that go way beyond its banal calls for “more exports”.

The question is how does a country unilaterally deal to this rort between multinationals and the tax advisory industry? The UK has had enough, it is not going to wait for an OECD consensus and has chosen to bring in a “diverted profits” or “Google” tax.[iii] This measure levies a 25% tax on profits deemed to be diverted out of the UK. Britain plans to accompany this measure by a 2% cut in the corporate tax rate to 18%.

Australia has yet to follow the UK’s “Google” tax precedent but has signalled greater surveillance over, and transparency requirements of, multinationals (including private companies) with annual turnover of more than A$200m.

The logical endpoint from failure on the part of tax authorities to ensure that foreign firms are on an equal footing with local firms is that local firms will relocate their head office overseas to enjoy the tax privileges afforded “foreign” companies. Even if these companies have no other sales apart from those in their home market, it can be worthwhile moving their headquarters abroad given the savings in tax. The US is battling this practice with several of its multinational corporates.

In aggregate, the amounts of assessable income being shifted are likely to be major and are just another demonstration that the biggest tax suckers in New Zealand are the taxed-at-source wage and salary earners (the equity argument) and that lost production opportunities for local firms ensue (the efficiency argument).

Unilateral action appeals because it brings this issue to a head sooner rather than later, possibly much later.

[i] http://www.oecd.org/ctp/beps-frequentlyaskedquestions.htm

[ii] Rob McLeod, op-ed April 2015, “Tax laws need a multi-lateral solution”, http://www.stuff.co.nz/business/opinion-analysis/67969456/rob-mcleod-tax-laws-need-a-multilateral-solution

[iii] HM Revenue and Customs, 2015, “Diverted profits tax “ https://goo.gl/jLZtLD

What could we do unilaterally?

In New Zealand foreign firms have a number of ways of avoiding the tax impost that they would face if they were New Zealand-owned. Some are due to regulatory weaknesses, others due to stratagems these firms employ to deliberately reduce taxable earnings. On the regulatory front there are weaknesses around the double taxation agreements that New Zealand is party to. In short they allow a foreign firm to avoid New Zealand income tax if it doesn’t have a “permanent establishment” here.[i] For online businesses in particular this is a no-brainer. The remedy lies in modernising these tax treaties.

Given the two common ways for foreign firms to shift taxable profits beyond the New Zealand tax jurisdiction – namely taking on debt-heavy balance sheets, or deploying transfer pricing on their inputs – there are two broad ways to proceed.

The first is relatively simple but arguably overkill. It would see the IRD deeming a profit for the company as a pro rata share of the company’s worldwide profit apportioned by its New Zealand share of global sales. Clearly for taxation purposes the “company” would need to be defined as the general group of companies behind the product or service, rather than any special purpose New Zealand subsidiary set up specifically for distribution here. That does give rise to identification issues and difficulties around partly foreign-owned local operations.

The second approach is to deal with the profit transferring behaviour of any foreign owned company operating in New Zealand. The remedies here comprise of two stratagems as follows;

1. Dealing with Thin Capitalisation

Leveraging up the balance sheet so that interest costs rise is an easy way to dodge tax – the interest is a deduction and it flows offshore to who-knows-where so the lender (a related party) can collect that money in a lower (sometimes zero) tax jurisdiction. New Zealand moved against this in 1996 by introducing thin capitalisation rules which in effect nowadays attempt to limit the amount of gearing to 60% of the balance sheet assets of the New Zealand-registered company.

Of course this still affords plenty of scope for tax dodging via debt and seems little more than symbolic. A more robust way of setting the gearing ceiling would be to get data on industry average gearing for the firm’s peers and set the ceiling at that level for all firms whose interest payments flow beyond our tax jurisdiction.

Our IRD would probably argue that would be too much hassle and that the 60% rule is quick and more-or-less effective. We’d suggest it’s lazy and that the default should be no interest-bearing debt from abroad is allowed unless the taxpayer is able to prove their claim that the interest is a legitimate cost. They could do this only if the debt met particular criteria; for example to get tax relief the taxpayer would have to produce the data on international gearing norms for their sector and, secondly, provide evidence as to why their gearing internationally should be higher than international norms. With this sort of regime the onus of proof for deductibility lies with the taxpayer, not the IRD.

If they can’t prove it they don’t get it.

2. Dealing with Transfer Pricing

The second tax dodge available for foreign companies is transfer pricing. Companies who play this game “purchase” an input from a related party that sits outside the New Zealand tax jurisdiction (often in a tax haven), effectively transferring their pre-tax profits to that party. Again the IRD does have a policy on this, it’s a policy that reflects our signing of international double tax treaties with other OECD countries. But the reality is it doesn’t work, we are sitting ducks. Multinationals can shift profits away from where the economic activity occurs to where the tax liability is minimised. Examples are abundant – Coca Cola, Facebook, Apple are just examples of multinationals operating in New Zealand whose practices have come under fire because their tax liabilities are significantly and consistently lower, year after year as a percentage of sales, than any comparable firms operating solely in New Zealand. Prima facie there is certainly a case to put the onus of proof of compliance on these firms.

In order to shut down transfer pricing practices firms should pass three eligibility tests before being allowed to claim the costs of imported inputs (materials, royalties, interest, licence fees) as deductible expenses. Importantly with these tests, the onus of proof for deductibility would fall on the taxpayer, and not be up to the IRD to prove an expense didn’t qualify. If the corporate can’t provide the proof then the costs simply are not deductible for the purposes of stating New Zealand taxable profits.

The first test for tax deductibility would be proving that the input being purchased from a non-New Zealand party is not from one that has a beneficial foreign shareholding of say 5% or more in common with the taxable company. ‘Beneficial’ covers direct and indirect (through third parties) shareholdings.

The second, and additional hurdle would be requiring the tax payer to establish that the cost of the input is no higher than would occur in an arms length transaction between non-related parties.

If the taxpayer cannot establish Test 2 because of lack of comparable industry data (such might be the case for a royalty for IP say) then the third test is for the taxpayer to establish that the royalty is no more than parties pay for the use of that IP in the IP owner’s country. And if the IP owner’s country is a tax haven then the taxpayer has to use as their benchmark the average of 3 white list countries to establish the absence of price-ramping.[i]

Finally, as an alternative to the eligibility tests above, the multinational could instead establish its taxpayer bona fides by simply proving that its overall tax burden across all the white list countries it operates in, is no lower than industry averages. This alternate method demonstrates that the New Zealand tax impost is intended to be no higher (or lower) than the average of white list jurisdictions.

This blog was an excerpt from the Morgan Foundation report New Zealand Income Tax: Unfair and Favours the Rich

[i] Pearce Trust Blog, November 2012, “What is a White Listed Country?” http://www.pearse-trust.ie/blog/bid/91500/What-Is-A-White-Listed-Country

[i] http://www.stuff.co.nz/business/opinion-analysis/78217846/Craig-Elliffe-Double-tax-treaties-are-the-toughest-nut-to-crack